5 Tips for Homebuyers Who Want to Make a Competitive Offer

5 Tips for Homebuyers Who Want to Make a Competitive Offer Today’s real estate market has high buyer interest and low housing inventory. With so many buyers competing

Will Mortgage Rates Remain Low Next Year?

Will Mortgage Rates Remain Low Next Year? In 2020, buyers got a big boost in the housing market as mortgage rates dropped throughout the year.

Why Working from Home May Spark Your Next Move

Why Working from Home May Spark Your Next Move If you’ve been working from home this year, chances are you’ve been at it a little longer than

Is it Safe to Sell My House Right Now?

Is it Safe to Sell My House Right Now? In today’s real estate market, the buzz is all about how it’s a great time to

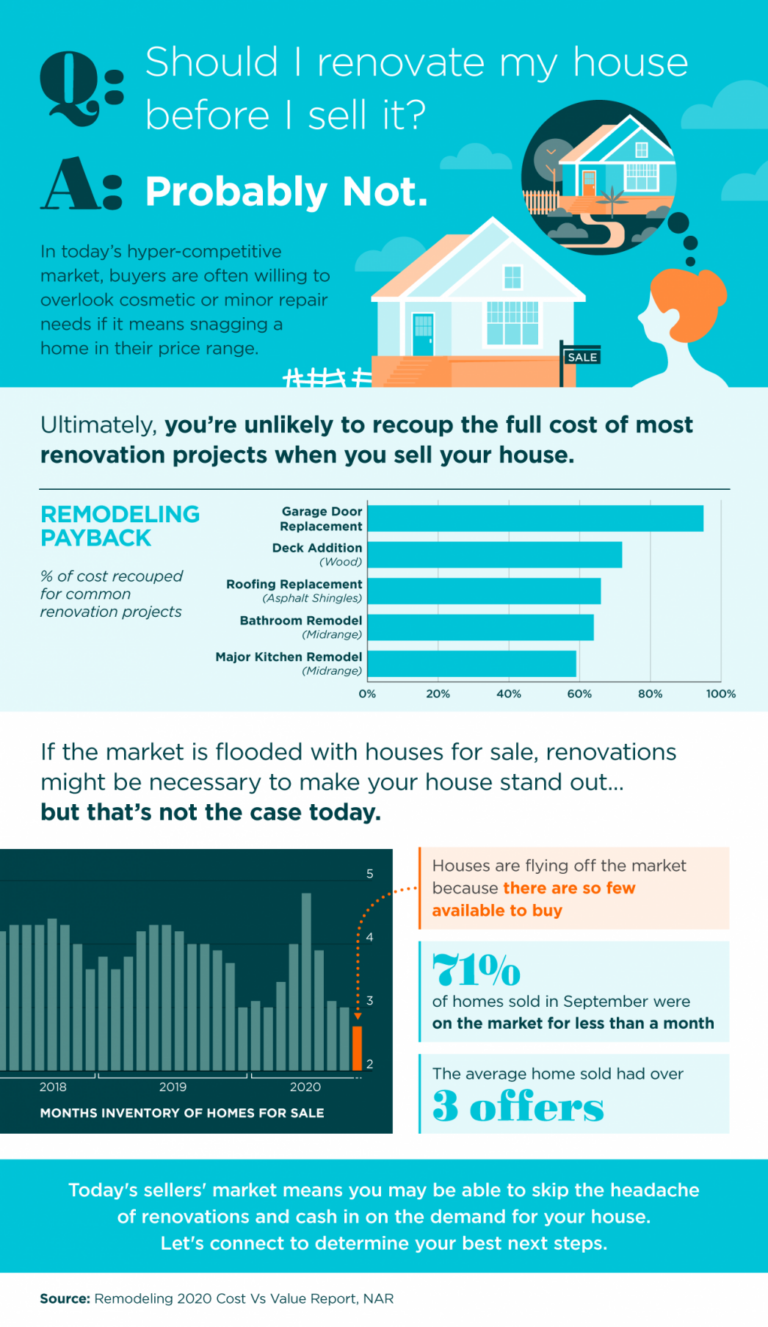

Should I Renovate My House Before I Sell It?

Should I Renovate My House Before I Sell It? Some Highlights In today’s hyper-competitive market, buyers are often willing to overlook cosmetic or minor repair

Selling Your House Is the Right Move, Right Now

Selling Your House Is the Right Move, Right Now [INFOGRAPHIC] Some Highlights Demand from homebuyers has skyrocketed this year, which means today’s sellers are poised

The #1 Reason Not to Wait to List Your House for Sale

The #1 Reason Not to Wait to List Your House for Sale Many industries have been devastated by the economic shutdown caused by the COVID-19

6 Reasons You’ll Win by Selling with a Real Estate Agent This Fall

6 Reasons You’ll Win by Selling with a Real Estate Agent This Fall There are many benefits to working with a real estate professional when

Atlanta Turtle Group

404.551.2607

info@AtlantaTurtleGroup.com

Keller Williams Metro Atlanta

315 W Ponce De Leon Ave, Suite 100

Decatur GA 30030

404-564-5560