Where Are Home Values Headed Over the Next 12 Months?

Where Are Home Values Headed Over the Next 12 Months? As shelter-in-place orders were implemented earlier this year, many questioned what the shutdown would mean

Why Selling this Fall May Be Your Best Move

Why Selling this Fall May Be Your Best Move If you’re thinking about moving, selling your house this fall might be the way to go.

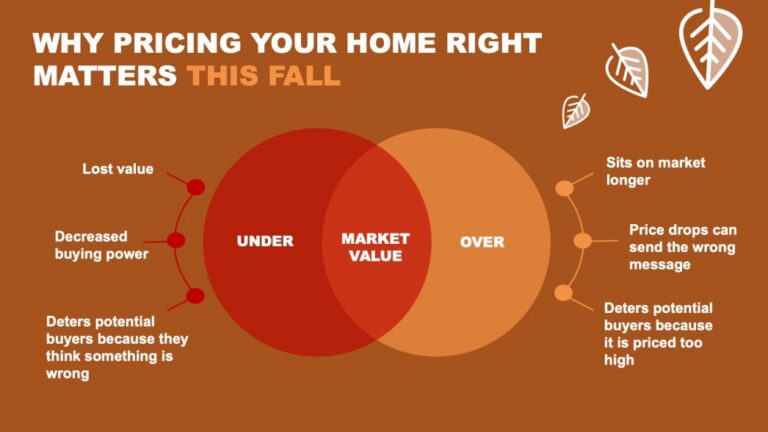

Why Pricing Your Home Right Matters This Fall

Why Pricing Your Home Right Matters This Fall Some Highlights As a seller today, you may think pricing your home on the high end will

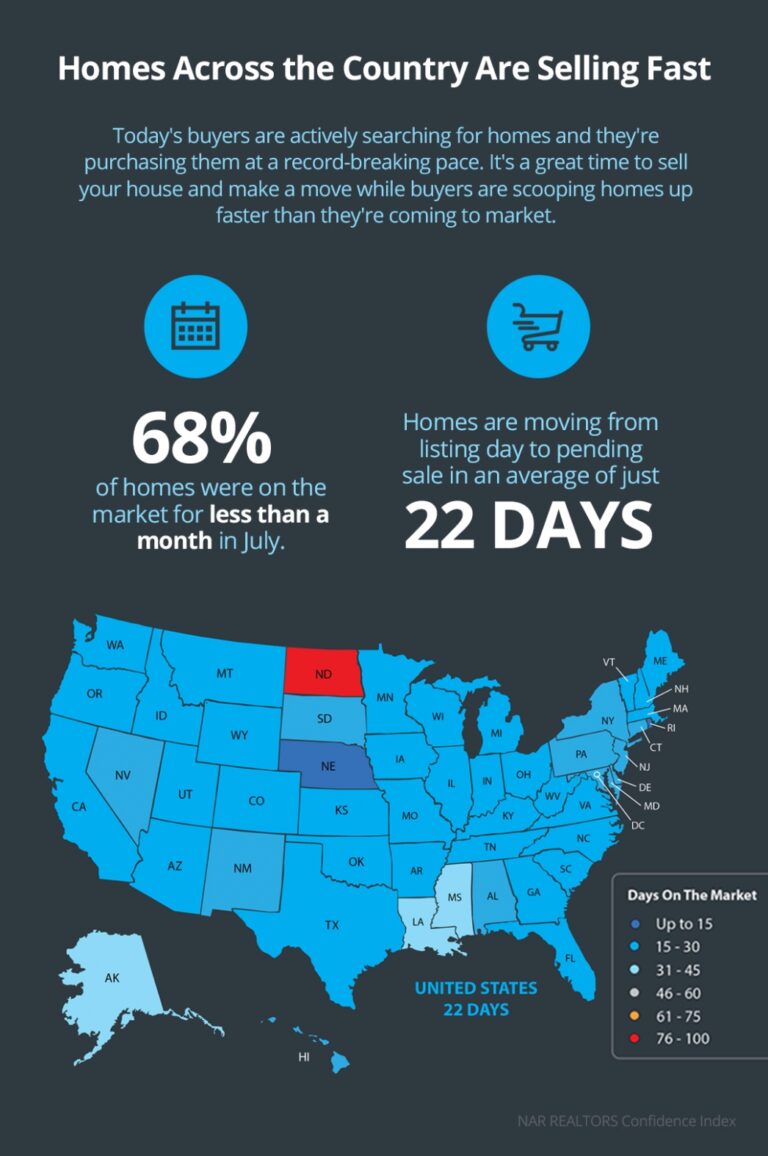

Homes Across the Country Are Selling Fast

Homes Across the Country Are Selling Fast Some Highlights Buyers are actively searching for and purchasing homes at a record-breaking pace. According to the latest

How Low Inventory May Impact the Housing Market This Fall

How Low Inventory May Impact the Housing Market This Fall Real estate continues to be called the ‘bright spot’ in the current economy, but there’s

Homebuyer Demand Is Far Above Last Year’s Pace

Homebuyer Demand Is Far Above Last Year’s Pace Homebuying has been on the rise over the past few months, with record-breaking sales powering through the

Builders & Realtors Agree: Real Estate Is Back

Builders & Realtors Agree: Real Estate Is Back When shelter-in-place orders brought the economy to a screeching halt earlier this year, many believed the residential

The Top Reasons People Are Moving This Year

The Top Reasons People Are Moving This Year Today, Americans are moving for a variety of different reasons. The current health crisis has truly re-shaped

Atlanta Turtle Group

404.551.2607

info@AtlantaTurtleGroup.com

Keller Williams Metro Atlanta

315 W Ponce De Leon Ave, Suite 100

Decatur GA 30030

404-564-5560